Year-end accounting is a vital task for every small business. It ensures the maintenance of financial accuracy and compliance, and is ready for HMRC submissions. Some essential activities that are done before the closing of the fiscal year include reviewing expenses, updating financial records, preparing VAT documents, and verifying payroll details. It can prevent errors and penalties. A proper checklist of the necessary actions gives a better insight into the situation and great ideas for decision-making and financial planning for the following year.

If you too need to make preparations, avoid last-minute stress, maintain compliance, and start the new year strong and confident, then explore the article in detail.

Essential Year-End Accounting Tasks for Small Businesses

Year-end accounting in the UK is a review, update, and finalisation of the financial records of a company at the close of an accounting year. Usually, the year-end for most limited companies is 12 months from the date of incorporation; however, businesses may change it if they wish.

This is the mandated process by law for filing year-end accounts to Companies House and your Corporation Tax return to HMRC. However, it is also an excellent opportunity to check the financial health of your business, work on tax planning, and get ready for the next financial year-end.

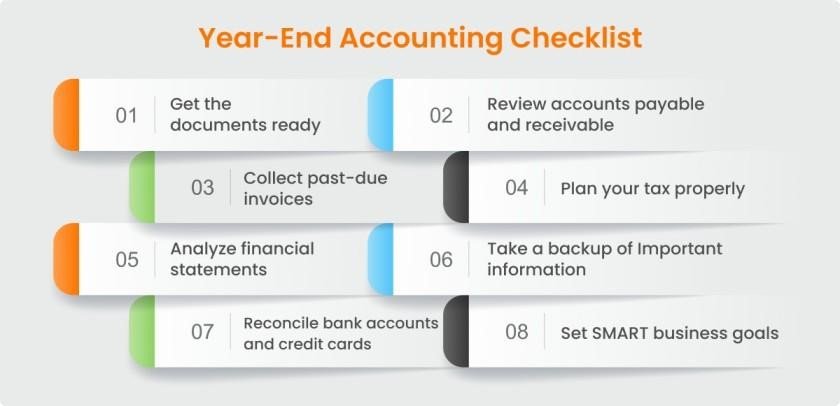

Understand Year-End Accounting Task to Save Time, Reduce Stress, and Keep Your Business Compliant

1. Match Your Bank and Card Transactions:

Reconciling bank and credit card activity is the first task involved in year-end accounting. You need to check what is recorded in the accounting system. This reconciliation process is essential for accurate year-end reporting. Download bank and card statements for the entire year and compare them with bookkeeping records to identify errors, duplicates, or missing entries.

2. Tidy Up Outstanding Invoices and Bills:

Unsettled, unpaid customer invoices and supplier bills may mislead the cash flow and tax position of the business. Review your accounts receivable, identify overdue accounts, and decide which you should write off as bad debt. In terms of payables, make sure that all supplier invoices, especially those covering the year-end period, are appropriately recorded.

3. Complete a Thorough Stocktake:

If you have a product-based business in the UK, it is essential to conduct a year-end inventory review. A physical stocktake should be carried out at the end of the year, and the figures should be reconciled with your company’s bookkeeping records. Remove any items that are expired, damaged, or obsolete from your inventory. This ensures accurate Cost of Goods Sold (COGS) calculations and helps prevent overpaying tax.

4. Check Your Fixed Assets and Depreciation:

You must know that year-end is the best moment to review your fixed assets, which essentially comprise equipment, vehicles, and technology. You should make sure that your fixed asset register documents all new purchases listed and that depreciation is properly recorded. Proper records ensure that you are claiming the correct Capital Allowances and are getting the best use of tax relief.

5. Verify Payroll and Employee Information:

Payroll accuracy is vital and heavily regulated. Examine the employees ‘ records, such as their working hours, bonuses, holiday pay, and contributions to pensions. The UK employers are obliged to make sure that their Real Time Information (RTI) submissions align with payroll journals. Before finishing the year, use a payroll tool to verify that PAYE, NICs, and other deductions are correct.

6. Review and Categorise Business Expenses:

Expense categories need to be precise and consistent so that they can match the HMRC regulations and to be able to claim all the allowable deductions. Examine your general ledger for transactions that have been incorrectly classified, especially in the areas of client entertainment, subscriptions, and home office expenses. Proper coding helps to avoid inflated costs and reduce the risk of an audit.

7. Record Final Year-End Adjustments:

Accruals, prepayments, depreciation adjustments, and bad-debt write-offs are vital to the process of your accounts depicting actual financial performance. Prepare your adjusting journal entries ready, along with the support documents, and make sure they are the last entries before producing final reports.

8. Generate Your Financial Statements:

After reconciling your books and posting journal entries, you can now prepare your financial reports. These are your Profit and Loss (P&L) statement, Balance Sheet, and Cash Flow Statement. These reports constitute the essence of your year-end accounts and represent a summary of your business performance.

Analyzing the figures of the current year against those of the past years is a good practice. Are sales increasing? Are profit margins getting better? Is your business excessively reliant on a few customers or suppliers? Financial analysis is a great tool to identify risks, discover new opportunities, and make long-term plans for the next accounting year.

The Importance of Expert Help During Year-End Accounting

Year-end accounting is as vital as it is complex. It requires meeting multiple financial obligations. However, by seeking professional support at the right time, you can achieve complete accuracy in this task. Join the ASK group to make your year-end accounting task stress-free. AskGroup provides you with a full suite of accounting, compliance, and advisory services, ranging from bookkeeping, VAT returns, payroll, and year-end accounts to corporation tax filings and statutory returns.

By partnering with experts like AskGroup:

- Everything is taken care of with proper bookkeeping, VAT, payroll, and statutory account preparation; no need to look elsewhere.

- In case it is required, you can also get business advisory and strategic financial planning support (e.g., virtual CFO services, growth forecasting, budgeting) to help your business grow.

- You are safe from late-filings, errors, and compliance traps, thus giving you peace of mind during the busiest business time of the year.

Conclusion

Properly planned and year-end accounting will assist small businesses in maintaining compliance, being organised, and having a financial position that is ready for the coming year. It is essentially the cycle of a company that starts with account reconciliation, expense review, financial statement preparation, and then tax planning. Each of these steps is a powerful tool in a business’s monetary journey. By being proactive and detailed, you can avoid costly mistakes and receive insights that are instrumental in making better decisions and achieving sustainable growth.

If you are looking for a professional to support you in making your year-end accounting less hectic and more enjoyable, AskGroup is the right place to go. They provide expert services that are tailored to the needs of businesses in the UK, enabling them to be compliant and confident financially.